State of the Industry Report: U.S. EV Fast Charging — Q1 2025

Reliability is improving, the size of charging stations are growing in size, and average utilization rates have reached 25+% in several markets, according to the new State of the Industry Report: U.S. EV Fast Charging — Q1 2025, from Paren Inc.

Offering an in-depth analysis of the evolving electric vehicle DC fast charging (DCFC) landscape, the Q1 2025 report marks the beginning of a new series that aims to provide ongoing insights into deployment trends, utilization, reliability, pricing, and the state of key players in the fast-charging EV ecosystem.

Key Findings:

Reliability: Paren’s U.S. Reliability Index measured an improvement versus Q4 2024 of 81.2 points to 82.6, an increase of 1.7%. This continues a quarterly trend across the U.S. non-Tesla fast charging infrastructure, which suggests that the ongoing efforts to replace or sunset older hardware is having a positive impact on station uptime. In addition, newer entrants into the field are bringing time-tested hardware along with enhanced driver experiences.

“Despite some high-profile setbacks, the industry made real strides last year,” said Bill Ferro, CTO at Paren. “Paren’s U.S. Reliability Index measured an improvement versus Q4 2024 of 81.2 points to 82.6, an increase of 1.7%. This continues a quarterly trend across the U.S. non-Tesla fast charging infrastructure, which suggests that the ongoing efforts to replace or sunset older hardware is having a positive impact on station uptime. In addition, newer entrants into the field are bringing time-tested hardware along with enhanced driver experiences.”

Station and Port Growth: Total new ports (charging connections) grew to 55,580 at the end of Q1, an increase of 3,667 and stations (locations) reached 10,839, an increase of 794 in Q1. The number of new ports and stations added in Q1 were fewer than in Q4 2024 — a normal seasonal trend resulting from winter weather slowing construction in Q1, following year-end rushes to open new stations.

Utilization: Average utilization (minutes of charging session time as a percentage of time a station is open each day) across the U.S. also declined slightly to 16.2% from 16.6% in Q4 2024. Q1 2025’s small decline is a result of the typical Q4 bump caused by growing EV travel during the Thanksgiving and Christmas travel periods. However, utilization is trending up, especially in dense urban coastal markets with high rideshare and apartment renter households that depend on public charging. In fact, several markets such as Las Vegas, Miami, New York, Tampa, and Los Angeles are seeing average utilization rates around 40% during peak charging hours of the day.

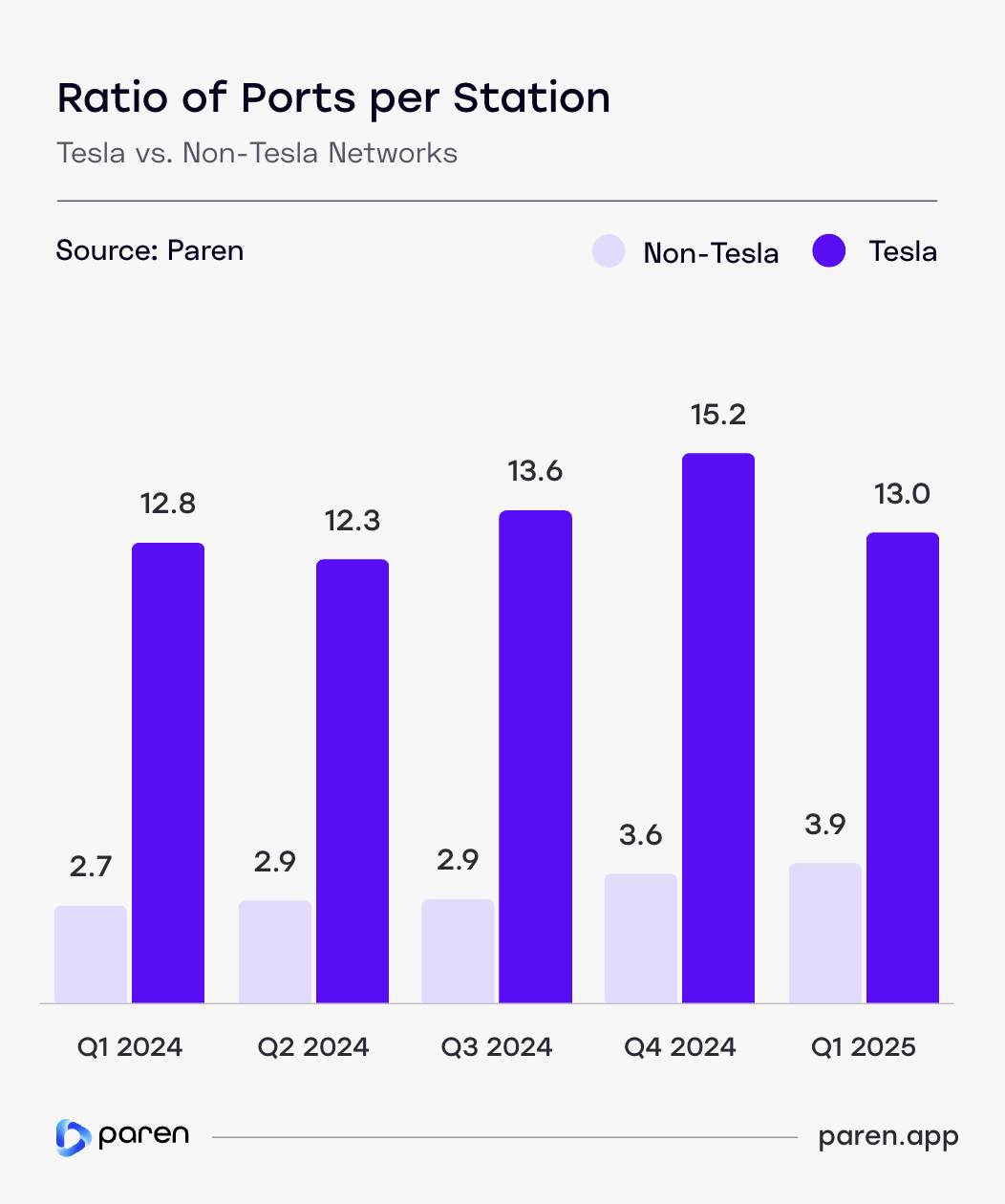

Ports to Stations Ratio: A significant and encouraging rise in the average ratio of ports per station among non-Tesla networks to 3.9 from 2.7 in Q1 2024. For context, the Tesla Supercharger network now averages 13.0 ports per station, and the National Electric Vehicle Infrastructure (NEVI) program requires a minimum of four ports per station.

NACS Connector Adoption: 59% of new ports added in Q1 2025 were CCS-enabled, 31% NACS-enabled, and 10% CHAdeMO. However, only 104 of the newly added NACS (J3400) ports were at non-Tesla networks, showing the U.S. is still in the very early stages of the transition to the J3400 connector standard — meaning drivers of new non-Tesla vehicles coming to market this year with a NACS port standard will need to heavily rely on adapters.

Pricing Models: Fixed pricing is being used by charge-point operators (CPOs) 80% of the time across the states, with the Time of Use (TOU) approach averaging 16%, and Time (e.g., by the minute or hour) rarely used at 4.2%. California is only state where use of TOU rates exceeds 50% of stations.

Of significant concern to the industry and EV drivers is the potential negative impact of an extended pause of the NEVI program, which was designed specifically to fund the build out of charging infrastructure in rural and low-income communities where charging networks are typically not building new charging stations. Our data is a harbinger of a “charger divide” as CPOs will increasingly focus on urban markets seeing high utilization, often north of 30%, versus markets with less than 5% utilization.

View online or download a PDF of the report (registration required)

Author: Loren McDonald, Chief Analyst